I hope by now I’m starting to get through to people about online identity management, because here in the UK a whole lotta folk are about to be forced to sign their life over to an Identity Provider. The UK government has decided to host all of its public services online, to fulfill the ‘Digital by Default’ strategy. The Government Digital Strategy is now expected to be up and running by April 2014. Five companies have been chosen to provide identity management for UK citizens, one of which, the Post Office, will serve as registration centers for biometric smart ID enrollment.

When I try to tell people about this, and how it’s a global scheme, they just don’t seem to hear me. I can only think that the power of the media is responsible – they simply aren’t informing the public properly about this matter, so because you’re only hearing it from me, it perhaps doesn’t seem as real?

Well, it is.

Horribly so.

There aren’t any glossy adverts for it yet, but if you wade through the documents, and listen to lectures and webinars aimed at industry professionals, it’s all there on the Web.

Educating the public seems to have been ruled out, and instead, people are being drawn in by only being able to access certain services by using an Identity Provider (IdP) - this rules out debate, and the right to be informed. In the US, Obamacare and access to personal electronic health records will kick off national IdM take-up, while in the UK, it’s beginning with access to government services. No matter how private you’re told IdM makes you, there will always be an audit trail, and a host of exemptions from peeking.

Maybe you’re already one of the many victims of the transition to AI government – those wishing to claim Jobseeker’s Allowance must already make their claim online. It is not possible to do this by interacting with a human in any way.[1]

The thing is, the next stage is forcing people to sign up with an Identity Provider (IdP) to prove they are who they say they are, when they use government services which are only available online. It was supposed to start next month, i.e. the transition to Universal Credit (the new benefit which will replace most of the current ones) was meant to introduce identity management to the UK, by requiring all claimants to authenticate themselves online by using an IdP.

However, the plan has now changed, and the latest news is that instead of starting with Universal Credit, there will be 25 government departments moving their services online, and to access these, citizens will need to sign up with an Identity Provider. The services include online driving licences, and other DVLA documents; State benefits, redundancy payments, and tax matters; civil claims; visa applications; electoral registration; and booking prison visits.

In June, the government announced,

HM Revenue & Customs (HMRC) will become the first central government department to use Identity Assurance (IDA), one set of secure login details to access all online public services, and will be a key component of Pay As You Earn Online (PAYE Online) which is to move to pre-launch mode in October 2013 with ‘wider IDA capabilities becoming available from October 2014′.

The Government Digital Service (GDS), which is developing IDA, has described it such: “Identity assurance is about providing users with a simple, trusted and secure means of accessing public services, so we are working hard to ensure that privacy is at the heart of the service we will provide to users.”

According to governmentcomputing.com, “IDA is set to become the default service for all government departments providing public digital services which require the citizen to confirm their identity.”

The move comes as part of the Cabinet Office’s strategy to move all government services online in order to save between £1.7bn and £1.8bn a year.”

They don’t want to provide staff to man phonelines, or offices –everything will be digitised, and for that you need smart ID.

The UK government (Government Digital Services, or GDS) announced this month they have contracted the services of five companies, and we get to choose which one to sign up with! Gosh, thanks! The five IdPs chosen by GDS for the UK are Experian, Verizon, the Post Office, Mydex, and DigIdentity; the first/beta phase is just about to start. There were supposed to be eight IdPs, but PayPal and Cassidian have deferred their involvement for the time being.

It was reported last week that a government spokesperson has stated, “Universal Credit remains part of the future delivery plans for the cross-government IDa Service in development at the Cabinet Office."

Last year, (September, 2012), the UK Cabinet Office published the Local Authority Review of “Citizen Online Identity Assurance” which acknowledged one of the issues in enforcing the system is that “citizen trust may be difficult to achieve”. Too right!!! It’ll be even harder once people realize how easily they can be spied on, the fact that biometrics aren’t reliable enough, and that many things can go wrong when allowing a third party to handle your ability to live a life. If your global ID doesn’t work, you can’t do a thing.

In June the Government and the UK's National Technical Authority on Information Assurance (CESG) also published new guidance on 'identity proofing' and verification. The guide sets out how businesses tasked with verifying the identity of individuals using Government services can achieve various levels of assurance about the identity of such users.

The ‘Privacy and Consumer Advisory Group Draft Identity Assurance Principles’ were also published in June, and were actually endorsed by Big Brother Watch and No2ID, but all pretense of privacy is washed away by the exemptions (the “Exceptional Circumstances Principle”), which mean privacy can be violated for the following reasons:

in the interests of national security;

public safety or the economic well-being of the country;

for the prevention of disorder or crime;

for the protection of health or morals,

for the protection of the rights and freedoms of others.

This list kinda covers every excuse under the sun don’t ya think? Besides, there’s always the audit trail, and a whole variety of types of data about you that will be looked at. According to Mike Bracken, director of the Government Digital Service unit (GDS) in the Cabinet Office,

“IA data includes “Personal data”, “Audit data, “Attribute data, “Identity data”, “Relationship data”; “Transactional data” and other “General data”….

"Processing” in the context of IA data means “collecting, using, disclosing, retaining, transmitting, copying, comparing, corroborating, aggregating, accessing”… etc

… Subject to any audit or legal requirement, the Minimisation Principle requires any aggregation, correlation or corroboration to be of a transient nature. Any decision that requires a risk assessment of the Service-User will need the correlation of data from possibly a number of sources.”

The UK has contracted its e-Gov services to one company, owned by only one man, who will host the services in the cloud, using software it has contracted from EMC Global Services, an American corporation. Does this mean the UK government is granting control of all her citizens to a private US company?

Identity management enables full personality profiles for each of us, with a unique ID number, which works worldwide, using, for instance, the standards of the Open Identity Exchange (OIX) and ISO certification.

Chris Ferguson, the man in charge of ‘Identity Assurance’ here in the UK, is on the board of directors of the OIX.

In a workshop called ‘Comparing and Contrasting NSTIC with EU Approaches’ at this year’s World eID Congress, Chris Ferguson is due to give a presentation with the provisional title of “UK, a Laboratory for NSTIC in Europe”. this aligns with Ferguson’s commitment to working with his counterparts on his trip to the White House Colloquium on the NSTIC in May of last year, when the Cabinet Office noted,

The internet doesn’t stop at national borders and nor will the identity ecosystem. Identity services and the technical and legal environments in which they work will need to align internationally over time even if there are differences from one country or business context to another. A step closer, perhaps, to an International Strategy for Trusted Identities in Cyberspace?

In March, the Open Identity Exchange held a summit at the Microsoft headquarters in London, where Stephen Ufford, the founder of Trulioo (partnered with Verizon to deliver IdM in the UK, the US, and elsewhere) discussed the “problem” in the UK of the five million “unbanked” people – mainly the young and the old – who are classed as being “thin-file” people. Ufford also stated that instead of trying to “educate the public”, citizens could be “eased in” by getting them to use government services online. Trulioo specialises in social ID verification, and Ufford insists the government intends for us to use “social sign-ins” to begin with, such as through Google or Facebook, which would allow them to, “leverage existing consumer behaviour …. to make the verification process more simple”. The social (identity) file, he says, can include an email address, phone number, and even the device ID, and is, “created and aggregated just like a credit file. It’s reported from different identity providers, different instances of your social behaviour….”.

Speaking at the Japan Identity and Cloud Summit , Ufford said that only 5% of e-commerce websites use social log-ins at present, but experts expect that over the next three years, this number will rise to over fifty per cent. He also assured the corporate attendees that they needn’t worry about using Trulioo’s product (called ‘Profile Plus’) because, he said, “… this process (the data we’re using to verify the identities) is completely unregulated so you don’t have to worry about the various types of privacy legislation around the world.” Trulioo gathers all of the bits and pieces of your digital footprint and assembles them as an ID, to provide “internet life verification”, i.e. to ‘prove’ the person is still alive.

Don Thibeau, Founder of the Open Identity Exchange, and involved in setting up the NSTIC, believes the global identity ecosystem could use social and transactional information from the web and “repurpose it for other applications”. Perhaps he’s thinking of how much identity profiles are worth to marketers, financiers, researchers, and politicians.

A webinar by a company (Janrain) partnered with Trulioo (see above), called ‘Leveraging Rich Social Profile Data for Advanced Segmentation’, stated Janrain could get rich profile data, e.g. photo, address, and psychographics, as well as relationship status, declared interests, movies, sports, and even “explicit access to their friends graphs”- this would give marketing companies “close to a 360 degree view” of customers and “could enable one to one marketing” using “centrally stored personality data”.

The UK government guide for businesses, ‘Identity Proofing and Verification of an Individual’, describes the four levels of identity verification; a social log-in is the lowest level of authentication, as it is only ‘level 1’ and no evidence is obtained to verify the claimed identity; a level 2 identity has “sufficient evidence …. for it to be offered in support of civil proceedings”; a level 3 identity has been physically identified, meaning the owner of that identity has provided “sufficient confidence for it to be offered in support of criminal proceedings”; whilst the highest level of identity verification adds biometrics, “to further protect the identity from impersonation or fabrication.” A level 4 identity biometric is “a measure of a human body characteristic that is captured, recorded and/or reproduced in compliance with ICAO 9303”.

The guide also notes that the following documents may be used, alongside other evidence, to authenticate a level 4 identity:

Biometric passports that comply with ICAO 9303 (e-passports) and implement basic or enhanced access control (e.g. UK/EEA/EU/US/AU/NZ/CN)

NHS staff card containing a Biometric

UK biometric residence permit (BRP)

UK asylum seekers Application Registration Card (ARC)

EEA/EU Government issued identity cards that comply with Council Regulation (EC) No 2252/2004 that contain a Biometric

The government’s Midata initiative, which requires businesses to compile “consumers' consumption and transaction data in a portable, machine readable format” is very close to being made compulsory for all businesses.

Midata was developed by the Department for Business, Innovation & Skills (BIS), “using insights and evidence from the Government’s Behaviour Insights Team in the Cabinet Office”.

The scheme is already compulsory for the energy, credit card, current account and mobile telephony sectors, but if secondary legislation is passed, all companies would have to comply. It is said to benefit consumers, but it will also facilitate ID authentication for thin-file people, since it is transactional data, and will make all audit investigations of ID far simpler.

Our health records will be regularly scrutinised by algorithms trying to understand such things as the spread of disease – for this a full ID profile helps ‘make sense’ of each record. Our profiles will also be collated and spread around by marketers, looking for the golden all-round view of who we are, to create a personalised consumer bubble for each of us.

We’re told the UK government won’t have a database of our IDs, but centralisation is no longer the issue – it is the ability to access and aggregate information from across the World Wide Web in real-time that counts, and ‘Identity Assurance’ does precisely this. Worse still, it moves our IDs to the cloud, where we are even less protected by law, leaving us vulnerable to companies from the US, a country which believes it has the right to snoop on us for the sake of ‘national security’. IdA just makes it easier for them.

The ‘Privacy Principles’ make it clear our IDs can be checked to ‘prevent crime’, which is effectively giving full clearance for all citizens to be surveilled, just in case.

Spread the word and don’t give in – right?

Notes:

[1] They then get you into the Job Centre and inform you that you MUST upload your CV (your identity profile) to a ‘government portal’ (called ‘Universal Jobmatch’) so prospective employers may browse them; so you can be monitored to ensure you really are trying to find work; and so the AI system can ‘match’ you with a job. Not having access to the internet is no excuse, and those who do sign up to Universal Jobmatch at home, are probably unaware that one particular cookie will be placed on their device for a full 1000 days. All this is managed by the Monster Corporation. Nice.

Jobseekers are also told “you must tell us if you leave your home, even if only for a day”.

Big Brother Biometrics ~ Coming to a Post Office Near You Soon

Paying for your own slavery was never so easy!

by Neil Foster | CPG Hub | Friday, 20 September, 2013

If our parents and grandparents hadn’t fought in two World Wars to ensure that Fascism or Nazism didn’t come to

the shores of Britain then, although a little sceptical, we may have accepted the advances in technology being used by successive governments as benign and an addition to our way of life that was not only beneficial to the users of such technology but also of use to the government who are supposedly there to serve their public and who would use such technology in that context and in a manner which could be seen to be clearly advantageous to the general public.

However, they did fight and die in their millions to keep future generations free from such despotic tyranny.

They must must be turning their graves to see how far we've moved in that direction without a shot being fired or indeed not even a whimper of protest being heard.

The fact is that governments in the following decades since the end of World War II have shown that they are neither there to serve or are in reality benign in any shape or form. They simply cannot be trusted with anything with regard to the welfare of the public. We only have to look at the crumbling infrastructure in every city in the country and the connecting transport facilities between high density areas to see the degradation which has taken place in recent times. Our health ‘service’ has become a dysfunctional shadow of its former self, with thousands of unnecessary deaths occuring every year, as has every other emergency service in the country with more rapid moves towards the privatisation of those services in the pipeline to further erode their efficiency and cost benefit to the end user, who over

generations has been taxed exorbitantly to pay for the growth of these services only to see them pawned off to shadowy friends of the ruling elite using our so called ‘elected’ representatives as the front men and women to convince the public that this is all such a great idea and will save us all hard earned cash… blah, blah, blah.

Yes, we’ve heard the rhetoric many times before and suffered the consequences of our apathy in allowing all of our utilities to be sold off at bargain basement prices only to be fleeced by the corporate giants who now own them.

Where’s the outrage? Where’re those MP’s to fight for our rights to the means of survival we once had for free and to whom we pay lavish salaries and lifetime index linked pensions for a paltry 5 years of uselessness dressed up as ‘serving the community’? Can anyone really still believe that these parasitical prostitutes work for us?

I’m sure many of us still remember the local village Post Office where people used to queue up and chat to their neighbours whilst they did their bits of business, buying stamps etc.,

Those have now almost disappeared to be replaced by city location multi service cattle pens for the herd to access a range of ‘products’ as they are now termed.

The video below is the latest product to be brought online and if this doesn’t cause outrage then anyone who foolishly pays to become part of this global electronic surveillance gulag being peddled here deserves all they get in the near 'Utopian' future.

And if you still think this is just a convenient way of accessing what was once your right as a British citizen, to use that slogan, and which was once free access, then perhaps the following video will shake you from your comatose stupor making you realise the sinister agenda being rolled out here and the consequences of it in the hands of a government who will use such means against its own citizens. The Nazis would have loved this kind of power; the power to exclude anyone from any area of life it chooses.

And if you think this is all simply about accessing government ‘services’ please bear in mind that so called ‘government services’ are being privatised at such an alarming rate that there will be no such thing in the future where all what were once ‘services’ become commodities which can only be accessed if you have the ability to pay for them.

It doesn't matter how childishly the Post Office speaks to you in their advert or the happy clappy music makes you feel in the UK.gov advert... This is a totalitarian surveillance system being rolled out across the country and the wider world. You will be tracked through it wherever you feel 'free' to go... Now isn't that an oxymoron!

In the future all of your information will be linked to this system; your bank account balance, your vaccine history and general medical records, no vaccine, no access, what groceries you've been purchasing and all other items you buy. Your private insurance cover, which you'll soon be forced into paying for too, will definately be linked so that when you pick up those chocolate biscuits that you're so fond of off the shelf in your "oh so friendly", "every little helps" supermarket and you use your loyalty card when paying for them your 'Big Pharma' sponsored 'doctor' will be alerted. What do you think the response of your local privatised health clinic will be when you seek their help for any minor ailment?

Computer says NO!

Of course, that's assuming that you'll be allowed into the supermarket in the first place as you're biometrics will be scanned well before you even get to the entrance.

You better hope you've not upset anyone who may have the power to shut you down, like your local MP... That Manipulative Parasite who's never worked for you or any of his or her constituents and who couldn't care less if biometrics were used to starve you to death.

Welcome to the digital gulag... You will be assimiliated... but only if you're foolish enough to comply!

Ironically, i've also got a bit of info that neither covered. I know the company that is behind it.

American company called 3M. Sort of a bit like Capita.

I've just double checked and these webpages have been removed since i last visited them... Getting 404 Errors

3M provides solutions for its government and commercial customers as they confront threats to individuals, physical assets, information and the communications infrastructure. 3M's biometric and software technologies also facilitate and authenticate the secure passage of travellers across borders. Includes respiratory protection products and training, health and first aid products, as well as protective materials. Additional products assist first responders in fire and traffic management and policing.

Market Solutions

Security Systems

We've helped more than 100 countries successfully implement security initiatives, from integrating security materials into their secure ID credentials to developing full solutions from enrollment to personalization and delivery of the credential. Our border control solutions are in place along major national borders, in the United Kingdom, from United States to Mexico, in Canada and China. We bring that experience to bear in helping you meet evolving security regulations and security challenges with complete solutions.

Passport Issuance Passport Issuance

Our comprehensive offering includes everything from software, hardware and material solutions to a full-service passport production facility.

Border Management Border Management

From integrated border management systems to e-passport readers, our solutions are designed to deliver fast travel document validation in real time.

Driver's License & ID Card Issuance Driver's License & ID Card Issuance

We offer end-to-end driver's license and ID card issuance solutions that are not only secure, but also easy to authenticate.

Law Enforcement Law Enforcement

We help meet the needs of law enforcement agencies by providing biometric identification solutions that are cost-effective, FBI-certified and fully NIST-compliant.

Tax Stamp Tax Stamp

We offer a broad portfolio of technologies and expertise in security printing to bring you customized, secure tax stamp solutions.

Brand & Asset Protection

We design our solutions to move more information in real time, helping you capture and process passenger and customer data securely, accurately — and efficiently. With increased security requirements for airlines and regulation requirements for hospitality, gaming and financial services, we understand your needs to stay compliant and your needs to provide customer service.

Airline Check-in Airline Check-in

Our family of document readers and software solutions is SITA- and ARINC-certified and can easily integrate with your traveler processing applications to help more passengers move quickly from check-in to boarding.

Customer Indentity Solutions Customer Identity Solutions

Our proven solutions can easily integrate with your processes to help provide fast, accurate and easy-to-use data capture — so you can provide better customer service, help prevent fraud and stay in compliance with regulations.

Security Labels Security Labels

Our label solutions are built on an extensive portfolio of overt and covert technologies that can be authenticated easily with or without tools — or in combination with tools for higher security.

Serialisation & Tracking Serialisation & Tracking

Our comprehensive supply chain solution gives you critical visibility throughout distribution and sales and allows customers to validate the authenticity of their purchase — plus captures consumer data, so you can build customer relationships and loyalty.

Buildings

3M Window Film Window Film

At 3M, our wide range of building safety and security solutions, including window security film, solar window films and fire stop systems to prevent fire, and are designed to protect against crime, fire and damage to buildings, to increase building security.

Emergency Response

Products for Emergency Services Products for Emergency Services

Visit this section for helpful guidance on suggested products for Emergency Services and information on our range from Reflective Material to Hearing Protective equipment - all suitable for daily use by the Emergency Services.

Health & Safety

3M Personal Protective Equipment Personal Protective Equipment

We specialise in hearing and eye guards, and respirators to protect against dust and fumes, as well as reflective clothing for greater visibility, thermal clothing to keep in the heat and a select range of high quality stylish protective coveralls offering breathable comfort and protection you can rely on.

3M Signage/Graphic Films/Floor Graphics Safety-Walk

3M Safety-Walk offers a full range of floor level safety products to minimise risk in many industrial applications. They have been developed by 3M to provide effective, consistent and repeatable high performance levels over a long service life.

Office

3M Privacy Filters Computer Privacy Filters

Vikuiti™ Privacy Filters feature patented micro-louvre technology that blocks the view of a screen to everyone but the user sitting directly in front of it. Made from flexible, hard-wearing film, they're designed to fit easily on any LCD monitor or laptop.

3M Stationary Solutions Stationery and Office Equipment

Our range of office products and accessories will help you make your workstation a more comfortable, and productive environment.

We are the last generation with a voice and free will to change the course of history. Everyone connected everywhere – smart phones are to be the tools of the Smart World Order; bringing an end to physical cash, keys, drivers’ licences, etc. They are also intended to be used daily to validate identity in the new ‘trusted’ internet community. The phone, or the chip that links the user’s ID to the phone, then becomes too valuable to lose, and the only safe place is under the skin. Unless we refuse to comply….

It goes something like this:

1. Create a climate of fear.

2. Get everyone online.

3. Enable even the poor to carry a cell phone.

4. Get everyone to talk about RFID and biometrics: the first phase of acceptance is expectation.

5. Chip as many things and people as you can (phones, pets, clothing, etc.) to make it normal.

6. Set up a global ID system but keep it hush hush.

7. Promote implants for health and safety, so people think they’re good.

8. Make it so you can use your phone for everything, especially payments and proving identity.

9. How do we know it’s really you? Your biometrics please!

10. Cyber attack! Revolution! Please protect us!

11. The economy collapses….. cash is gone, and all payments are now digital.

12. Phones get lost and stolen; biometrics get spoofed; carrying a phone is such a bother – and Verichips are just easier all round….

But… “Pssst!! Rewind!”

Time to change our minds.

We don’t have to co-operate. Awake and determined, we refuse to sign up with an Identity Provider, and we refuse to pay for anything with a phone.

We make it plain: they can stick their NSTIC up their ***

Their planned revolution takes a different course:

http://www.youtube.com/watch?v=ddmQhIiVM48 http://localfuture.org The collapse of complex societies of the past can inform the present on the risks of collapse. Dr. Joseph Tainter, author of the book The Collapse of Complex societies, and featured in Leonardo Dicaprio's film The Eleventh Hour, details the factors that led to the collapse of past civilizations including the Roman Empire.

Joined: 25 Jul 2005 Posts: 18335 Location: St. Pauls, Bristol, England

Posted: Thu Jan 09, 2014 8:15 pm Post subject:

One Mainframe To Rule Them All is a breathtaking rundown of the human microchipping agenda. Concise and effective, it breaks down the coming global information control grid in all its horrifying detail. Scarier than any horror movie could be because it is real and documented.

(1) IT is very easy for a trusted professional to embed a microchip into you without you knowing - via an open wound (eg: in an operation, any intravenous needle) including dentistry needles, pill form). Also keep in mind here – once the implant is inserted it can have the capability to erase any memory of the event. It is also not uncommon for a victim to be drugged or induced into unconsciousness in their own homes after unforced break-ins have occurred.

(2) Microchips are not as easy as you think to be detected in the body as they are now often smaller than a grain of rice, so can easily go undetected or show as a UBO – Unidentified Bright object in an MRI x-ray or often termed as a foreign body (found inside your body)..

(3) Many individuals have had x-rays done that show implants within the body. But often find the records have gone missing from the medical practitioners’ office and mysteriously from the individuals’ home. Others have had x-rays done and found that they are given in-correct x-ray results back - eg: A victim that has a cracked skull from an old injury - gets an x-ray back showing they are clear and the old injury is not showing! The few that still have their x-rays showing implants - Find - No authorities are prepared to investigate who implanted these implants or where they originated from.

(4) Often when a patient presents him/her self at a medical establishment and asks for an x-ray to check for a microchip implantation - Find themselves being diagnosed as having paranoia or being delusional etc as:-

Involuntary implantation is not accepted,

As being a possibility,

By most professionals!

So no x-ray is done!

And the patient is left to find the money to seek a private establishment to do the x-ray

Again with a fear as to whether these professionals can be trusted.

Many known cases of illegal implantation have had severe health effects including:-

Electrical currents running into and/or through various body parts,

Electrical shocks to various body parts,

Electrical jolts to random body parts,

Deep pain/aches various body parts,

Burning sensations to various body parts (often internally),

Pressure in the head and various body parts,

Clicking/popping sounds in the head,

Heart problems, palpitations

Major organ failure,

Various cancers,

Involuntary body movements,

Forced speech,

Slow memory recall,

Erased memory of set periods of time,

Continuous headaches ( that pain killers cannot fix),

Ear aches, ear hums,clicks,

Piercing high pitch sound inside ears

Multiple Chemical Sensitivity/Electro-sensitivity

Sudden unconsciousness

Mimicked voices/conversations to the head - But no one is there - (Known as the auditory effect)

(Note: A victim doesn't always look as sick as they are)

Pain Relief - Techniques that help to alleviate pain/pressure/swelling in various body parts

Picture

NOTE:

These effects can take years to eventuate

or

May never eventuate in some

As it all depends who’s hands have access

To the remote controls

That link to the microchip

From an unseen Source

As victims complaints often sound bizarre

&

most of the past and present atrocities have been

kept out of media circulation - worldwide,

The public & many honest professionals don’t easily accept the fact

'That Governmental departments & employees

within the trusted Professional arena, are capable of doing...'

such

UNETHICAL ACTS!

Some know these atrocities exist but decide to keep silent,

Due to fears of repercussions - such as job loss.

While others often accept pay offs/grants in return to

KEEP SILENT!

Picture

This common occurrence also happened in many of the other-

unethical, Non-consensual experiments...

That took years to be acknowledged:–

Even though masses of victims reported their cases prior!

So I now introduce you to:-

International Center Against Abuse of

Covert Technologies

Created in 2012 to bring awareness to the general public and the legal systems around the world in regards to serious human rights abuses utilizing covert weapons technology like Microwave technology & remote influencing technology. Currently the International Centre Against Abuse of Covert Technologies are doing-

Stages of Testing

Stage 1: Preliminary testing for Radio Frequency emitting from the human body using

an RF scanner, to find sections in the body where (non-consented) microchip

implants are likely to be. At the same time they are also using a

Radio Frequency counter to record the type of frequency emitting.

Currently this testing has been carried out in various states across the U.S.A,

Europe & Germany and will eventually be carried out worldwide.

2012 As at March 2012 approximately 34% of those (with symptoms) in the preliminary

scan, came up positive of radio frequency emitting from selected regions of the

body. In this group approximately 99% had auditory symptoms.

In the General public population (those without symptoms) in the preliminary

scan - approximately 83.4% came up positive for radio frequency emitting from

selected regions of the body.

A consistency of specific sections of the body are showing up positive with RF

emission within the general public (with or without symptoms) scanned so far.

Another type of consistency of specific sections of the body - showing up positive

with RF emission is others whom have served in the military.

Stage 2: For those that have shown positive in stage one – now go on to get the appropriate

X-ray, MRI, C.A.T scan done on the body parts found to be emitting RF.

Stage 3: RF scanning is redone in a controlled environment such as a faraday cage to

prevent any possibility of the defense panel in court assuming outside frequencies

are effecting the results. Resulting in victims being able to present the court with

100% proof that radio frequency is coming from the implanted RFID

microchip/implant.

ICAACT Phase III Scanning of Mr. Magnus Olsson

(Released 6th August 2013)

Phase 3 report - Download the report in PDF format

Phase 3 report - Download the zip file containing documents referred to in the appendices

Picture

Video below of: Radio frequency testing & more information by International Center Against Abuse of Covert Technologies

Main website - Here

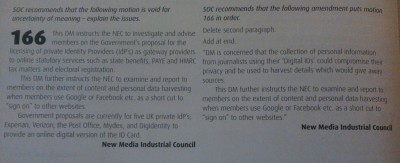

Good motion that 166 above! _________________ --

'Suppression of truth, human spirit and the holy chord of justice never works long-term. Something the suppressors never get.' David Southwell

http://aangirfan.blogspot.com http://aanirfan.blogspot.com

Martin Van Creveld: Let me quote General Moshe Dayan: "Israel must be like a mad dog, too dangerous to bother."

Martin Van Creveld: I'll quote Henry Kissinger: "In campaigns like this the antiterror forces lose, because they don't win, and the rebels win by not losing."

Motion 166 passed unanimously as amended.

Even managed to raise a laugh across the hall

"You thought we'd stopped the ID Card? Well it's back, it's digital, and it's already been privatised!" _________________ --

'Suppression of truth, human spirit and the holy chord of justice never works long-term. Something the suppressors never get.' David Southwell

http://aangirfan.blogspot.com http://aanirfan.blogspot.com

Martin Van Creveld: Let me quote General Moshe Dayan: "Israel must be like a mad dog, too dangerous to bother."

Martin Van Creveld: I'll quote Henry Kissinger: "In campaigns like this the antiterror forces lose, because they don't win, and the rebels win by not losing."

Joined: 25 Jul 2005 Posts: 18335 Location: St. Pauls, Bristol, England

Posted: Wed Jun 04, 2014 4:18 pm Post subject:

This week we go back to hear an update from a former correspondent, a single mum from North Wales, Julie Beal. She has been looking into the government's plans to get us all to have a universal digital ID, like the ID card we thought we'd successfully campaigned against only on-line. Julie explains what it will be used for: benefits; banking; HMRC Tax Returns... everything. And if you don't have the 'Open ID', 'Global Smart ID' or EID you won't be allowed to do it. Like many others Julie is worried that this technology will be migrated into the micro-chipping of humans in a slave-like fascist future UK.

http://www.getmindsmart.com http://www.activistpost.com

UK Orwellian Digital 'Smart ID' being imposed on us. Without it, young or old, you may starve. Julie Beal's update: http://youtu.be/jcYBBqFYAKI

Joined: 25 Jul 2005 Posts: 18335 Location: St. Pauls, Bristol, England

Posted: Sat May 16, 2015 9:35 am Post subject:

TMR 103 : Dr. Katherine Albrecht : RFID Implant Technology & The Mark of The Beast

Published on Friday, 20 March 2015 17:42

KatherineAlbrecht

This week we welcome Dr. Katherine Albrecht, privacy researcher, consumer advocate and bestselling author, who joins us for a wide-ranging discussion centred in her fascinating and compelling hypothesis that "the mark of the Beast" in the Book of Revelation might one day see literal fulfilment in the form of electronic identification devices implanted into human beings.

"He also caused everyone (small and great, rich and poor, free and slave) to obtain a mark on their right hand or on their forehead. Thus no one was allowed to buy or sell things unless he bore the mark of the beast – that is, his name or his number." (Rev. 13:16f, NET Bible)

Mindful of recent news that managers at an office block in Stockholm are inviting workers to receive RFID implants in the hand for the sake of ease and efficiency, Dr. Albrecht decribes her successful battle against the dangerous use of RFID implant technology, and explains how an experience of God in 1999 set her on the path of warning the world about the growing infrastructure of surveillance and control.

Dr. Katherine Albrecht is senior executive with the private search engines StartPage and Ixquick, is on the team behind the new privacy-protecting email program StartMail, and holds a Doctorate in Human Development and Consumer Education from Harvard University.

Human microchips took a big step closer today

£500 fine for those that don't chip their dogs

I remember the 1970s controversy over dog licensing. Nobody could understand why it was necessary? Many refused to get a licence.

All chip data will be on a privately owned database racket too which makes money every time you change your address

Some signs put up for lost dogs even include an admission they had microchips in them..! The ultimate irony is the promise the chip will help you get a lost dog back is a lie.

Toby Meyjes for Metro.co.ukTuesday 5 Apr 2016 1:41 pm

500

You've got less than 24 hours to chip your dog or face £500 fine

A new dog micro-chipping law comes in to affect on April 6 (Picture: Getty)

If your dog isn’t micro-chipped by Wednesday April 6 (yes, tomorrow) you could face a fine of £500.

A new law will come in to force which requires all dogs to have a chip inserted under their skin.

A racing greyhound who lived his life in the fast lane is now struggling to sniff out a loving home - because he is always ASLEEP

Jasper the greyhound can’t find a new home because he’s too sleepy

The aim is to make it easier to reunite lost dogs with their owners, which The Government says is costing councils and animal charities £57 million a year.

The latest estimate suggested that as many as one in five dog owners do not have their dogs microchipped, although this is likely to change.

Not complying with the law you could be landed with a several hundred pound fine.

Fines for not complying are as much as £500 (Picture: Getty Images)

Free microchipping is available at some local councils and several charities including the Dogs Trust, Blue Cross centres, Battersea Dogs and Cats Home.

The law

The Microchipping of Dogs (England) Regulations 2014 rule that all dogs, over eight weeks old, must have a chip.

The microchips will carry information about the animal that will be held in one of seven approved databases run by commercial operators.

Owners will have a responsibility to keep their information on the database up to date.

As database providers charge for a change of details some owners may be reluctant to keep the information up to date but failing to do so will incur a fine after April 6. _________________ --

'Suppression of truth, human spirit and the holy chord of justice never works long-term. Something the suppressors never get.' David Southwell

http://aangirfan.blogspot.com http://aanirfan.blogspot.com

Martin Van Creveld: Let me quote General Moshe Dayan: "Israel must be like a mad dog, too dangerous to bother."

Martin Van Creveld: I'll quote Henry Kissinger: "In campaigns like this the antiterror forces lose, because they don't win, and the rebels win by not losing."

Why you shouldn't microchip your dog, according to a leading vet

A leading vet has urged caution when it comes to microchipping (Picture: Getty Images)

In a few days time all dog owners will be required to get their pet microchipped by law.

But one leading vet has said doing such a thing could cause serious health problems and even lead to death in extreme cases.

Confused? Well, the advice is conflicting.

Richard Allport told Dogs Today the best approach is to ‘sit tight and do nothing’, while the Dogs Trust has called microchipping ‘essential’.

The senior vet, who owns the Natural Medicine Centre in Hertfordshire, said puppies are ‘far too young; to be microchipped at eight weeks – the new requirement by law.

He added: ‘Most of the serious adverse reactions (including death) have been in puppies and small breeds.

‘My advice to people who don’t want their dog’s microchipped is to sit tight and do nothing.’

On April 6 all dogs eight weeks and over have to be microchipped with owners risking a £500 fine for ignoring the new law.

epa05240976 Members of the public take part in International Pillow Fight Day event on Kennington Park in London, Britain, 02 April 2016. The Pillow Fight Day attracts tens of thousands people in more than 100 cities all over the world each year. EPA/WILL OLIVER EPA/WILL OLIVER

There WAS a pillow fight in London and some people took it more seriously than others

According to the Department for Environment Food and Rural Affairs around one in five dogs – 1.45 million – are yet to be chipped.

The procedure would see a microchip about the size of a grain of rice injected in to the animal’s shoulder blades. Each chip carries a 15 digit code.

Microchipping a dog costs between £10 and £30, but many charities, like the Dogs Trust do it for free.

Paula Boyden, veterinary director at the trust told the MailOnline ‘Losing a dog is an extremely upsetting time for both dog and dog owner and microchipping increases the likelihood that a dog will be reunited with its owner… making it an essential part of animal welfare law in England.

‘It is vital that the microchip details are kept up to date. Last year 47,596 unclaimed and unwanted dogs were left in council kennels across the UK as these dogs could not be reunited with their owners.’

There have been reported fatalities in the past that have been linked to microchipping.

But Pete Wedderburn, who is also a veterinary surgeon, said the benefits outweigh the risks.

He told the MailOnline: ‘It’s a big needle and big injection so naturally there’s going to be a reaction.

”But what you have to bear in mind is that this is looking at just one side – this is going to help with stray dogs and lives will be saved.’

https://www.youtube.com/watch?v=8Kep-ykqOvY _________________ --

'Suppression of truth, human spirit and the holy chord of justice never works long-term. Something the suppressors never get.' David Southwell

http://aangirfan.blogspot.com http://aanirfan.blogspot.com

Martin Van Creveld: Let me quote General Moshe Dayan: "Israel must be like a mad dog, too dangerous to bother."

Martin Van Creveld: I'll quote Henry Kissinger: "In campaigns like this the antiterror forces lose, because they don't win, and the rebels win by not losing."

Satan’s Credit Card: What The Mark Of The Beast Taught Me About The Future Of Money

Silicon Valley has sold us on a cashless, cardless, walletless, supposedly frictionless future — but as I learned living in it for a month, we’re not quite there yet.

https://www.buzzfeed.com/charliewarzel/yes-we-scan

Posted on May 21, 2016, at 4:50 p.m.

Charlie Warzel

It’s the dead of winter in Stockholm and I’m sitting in a very small room inside the very inaptly named Calm Body Modification clinic. A few feet away sits the syringe that will, soon enough, plunge into the fat between my thumb and forefinger and deposit a glass-encased microchip roughly the size of an engorged grain of rice.

“You freaking out a little?” asks Calm’s proprietor, a heavily tattooed man named Chai, as he runs an alcohol-soaked cotton swab across my hand. “It’s all right. You’re getting a microchip implanted inside your body. It’d be weird if you weren’t freaking out a little bit.” Of Course It * Hurts!, his T-shirt admonishes in bold type.

Anne Helen Petersen / BuzzFeed News

Chai and the writer at Calm Body Modification in Stockholm.

My choice to get microchipped was not ceremonial. It was neither a transhumanist statement nor the fulfillment of a childhood dream born of afternoons reading science fiction. I was here in Stockholm, a city that’s supposedly left cash behind, to see out the extreme conclusion of a monthlong experiment to live without cash, physical credit cards, and, eventually, later in the month, state-backed currency altogether, in a bid to see for myself what the future of money — as is currently being written by Silicon Valley — might look like.

Charlie Warzel / BuzzFeed News

Some of most powerful corporations in the world — Apple, Facebook, and Google; the Goliaths, the big guys, the companies that make the safest bets and rarely lose — are pouring resources and muscle into the payments industry, historically a complicated, low-margin business. Meanwhile, companies like Uber and Airbnb have been forced to become payments giants themselves, helping to facilitate and process millions of transactions (and millions of dollars) each day. A recent report from the auditor KPMG revealed that global investment in fintech — financial technology, that is — totaled $19.1 billion in 2015, a 106% jump compared to 2014; venture capital investment alone nearly quintupled between 2012 and last year. In 2014, Americans spent more than $3.68 billion using tap-to-pay tech, according to eMarketer. In 2015, that number was $8.71 billion, and in 2019, it’s projected to hit $210.45 billion. As Apple CEO Tim Cook told (warned?) a crowd in the U.K. last November, “Your kids will not know what money is.”

To hear Silicon Valley tell it, the broken-in leather wallet is on life support. I wanted to pull the plug. Which is how, ultimately, I found myself in this sterile Swedish backroom staring down a syringe the size of a pipe cleaner. I was here because I wanted to see the future of money. But really, I just wanted to pay for some * with a microchip in my hand.

The first thing you’ll notice if you ever decide to surrender your wallet is how damn many apps you’ll need in order to replace it. You’ll need a mobile credit card replacement — Apple Pay or Android Pay — for starters, but you’ll also need person-to-person payment apps like Venmo, PayPal, and Square Cash. Then don’t forget the lesser-knowns: Dwolla, Tilt, Tab, LevelUp, SEQR, Popmoney, P2P Payments, and Flint. Then you might as well embrace the cryptocurrency of the future, bitcoin, by downloading Circle, Breadwallet, Coinbase, Fold, Gliph, Xapo, and Blockchain. You’ll also want to cover your bases with individual retailer payment apps like Starbucks, Walmart, USPS Mobile, Exxon Speedpass, and Shell Motorist, to name but a few. Plus public and regular transit apps — Septa in Philadelphia, NJ Transit in New Jersey, Zipcar, Uber, Lyft. And because you have to eat and drink, Seamless, Drizly, Foodler, Saucey, Waitress, Munchery, and Sprig. The future is fractured.

This isn’t lost on Bryan Yeager, a senior analyst who covers payments for eMarketer. “This kind of piecemeal fragmentation is probably one of the biggest inhibitors out there,” he said. “I’ll be honest: It’s very confusing, not just to me, but to most customers. And it really erodes the value proposition that mobile payments are simpler.”

Charlie Warzel / BuzzFeed News

Venmo screenshot.

On a frigid January afternoon in Midtown Manhattan, just hours into my experiment, I found myself at 2 Bros., a red-tiled, fluorescent-lit pizza shop that operates with an aversion to frills. As I made my way past a row of stainless steel ovens, I watched the patrons in front of me grab their glistening slices while wordlessly forking over mangled bills, as has been our country’s custom for a century and a half. When my turn came to order, I croaked what was already my least-favorite phrase: "Do you, um, take Apple Pay?" The man behind the counter blinked four times before (wisely) declaring me a lost cause and moving to the next person in line.

This kind of bewildered rejection was fairly common. A change may be coming for money, but not everyone’s on board yet, and Yaeger's entirely correct that the "simple" value proposition hasn't entirely come to pass. Paying with the wave of a phone, I found, pushes you toward extremes; to submit to the will of one of the major mobile wallets is to choose between big-box retailers and chain restaurants and small, niche luxury stores. The only business in my Brooklyn neighborhood that took Apple Pay or Android Pay was a cafe where a large iced coffee runs upwards of $5; globally, most of the businesses that have signed on as Apple Pay partners are large national chains like Jamba Juice, Pep Boys, Best Buy, and Macy’s.

Partially for this reason, the primary way most Americans are currently experiencing the great fintech boom isn’t through Apple or Android Pay at all, but through proprietary payment apps from chains such as Target, Walmart, and Starbucks — as of last October, an astonishing 1 in 5 of all Starbucks transactions in the U.S. were done through the company’s mobile app. It wouldn’t be all that hard to live a fully functional — if possibly boring — cash-free consumer life by tapping and swiping the proprietary apps of our nation’s biggest stores.

If that doesn’t feel revolutionary or particularly futuristic, it’s because it’s not really meant to. But the future of mobile retail is assuredly dystopian. Just ask Andy O’Dell, who works for Clutch, a marketing company that helps with consumer loyalty programs and deals with these kinds of mobile purchasing apps. “Apple Pay and the Starbucks payment app have nothing to do with actual payments,” he told me. “The power of payments and the future of these programs is in the data they generate.”

“The power of payments is in the data they generate.”

Imagine this future: Every day you go to Starbucks before work because it’s right near your house. You use the app, and to ensure your reliable patronage, Starbucks coughs up a loyalty reward, giving you a free cup of coffee every 15 visits. Great deal, you say! O’Dell disagrees. According to him, Starbucks is just hurting its margins by giving you something you’d already be buying. The real trick, he argued, is changing your behavior. He offers a new scenario where this time, instead of a free coffee every 15 visits, you get a free danish — which you try and then realize it goes great with coffee. So you start buying a danish once a week, then maybe twice a week, until it starts to feel like it was your idea all along.

In that case, O’Dell said, Starbucks has "changed my behavior and captured more share of my wallet, and they've also given me more of what I want."

"That's terrifying," I told him.

"But that’s the brave new world, man," he shot back. "Moving payments from plastic swipes to digital taps is going to change how companies influence your behavior. That's what you're asking, right? Well, that's how we're doing it."

In this sense, the payments rush is, in no small part, a data rush. Creating a wallet that’s just a digital version of the one you keep in your pocket is not the endgame. But figuring out where you shop, when you shop, and exactly what products you have an affinity for, and then bundling all that information in digestible chunks to inform the marketers of the world? Being able to, as O’Dell puts it, “drive you to the outcome they want you to have like a rat in a maze by understanding, down to your personality, who you are”? That’s disruption worth investing in.

Jared Harrell / BuzzFeed News (2)

For all its complexity and bureaucracy and importance, money, at its core, is really just information. When FDR weaned the United States off the gold standard in 1933, cash, no longer backed by physical gold, became an abstraction. Today, that abstraction is pushed to new extremes: Not only does 92% of the money in the world exist as a series of ones and zeroes, but now it’s being transferred from place to place by any number of digital intermediaries looking to take a cut.

That process is complicated, but the key issue is trust. Money, argues David Wolman in The End of Money, is not much more than “a belief in a shared purpose, or at least a shared hallucination.” This faith in the “particular religion” of cash has been at the center of standardized currencies since Kublai Khan, and the loss of that faith has been associated with every major economic catastrophe in history. But trust — especially when it comes to new forms of currency — takes time to build.

The first two weeks of my experiment, most people balked when I offered an alternative means of payment. “I’m a little worried this might not go through in time,” one server at a German beer hall told me when I asked if I could Venmo her for my bill. A waiter at a different establishment scoffed when I tried to pay him or the restaurant via PayPal, suggesting his manager would think he was getting ripped off.

Yaeger sees this as standard for a nascent technology. “I kind of equate now to where things were 10 to 12 years ago with e-commerce,” he told me. “The concept of putting credit cards on a screen was new. Retailers and normal people were concerned about that. So innovative companies like PayPal and Amazon built that trust up over a decade while others slowly moved in.”

There are, of course, legitimate reasons not to trust these new forms of payment. Anyone who’s been mugged or lost a wallet knows cash is far from perfect, but this constellation of new digital payment products introduces a whole new category and scale of ways to get robbed, hacked, scammed, and screwed. Venmo — the social payment service that’s now transferring over $1 billion per month — may, in some ways, be the truest glimpse at a mobile payment future, but it’s not exactly entirely secure. Smartphones can be as easily lost and stolen as wallets, but they’re also eminently breakable, orders of magnitude more expensive, and obsolete after two or three years. And the payment-apps landscape is still such that living cashlessly in 2016 means entering your credit card information or routing number into dozens of stand-alone apps, some of which look as if they’ve been built overnight by a high school computer science class.

Charlie Warzel / BuzzFeed News

At the barbershop.

All this risk and all this friction, in the service of...what, exactly? “Plastic works really well,” Randy Reddig, an entrepreneur who was a part of Square’s founding team, told me, taking a shot at what he called “mobile wallet hysteria.” “I have a wallet right now in my pocket, and it’s great. It can feel like this is something that nobody is asking for. It’s solutioneering: Take something that exists just fine in the meatspace world and make it digital and somehow we’re all supposed to believe it’s better.”

To Reddig, the true future of payments is revealing itself inside many of Silicon Valley’s biggest new companies. Airbnb, he said, has one of the most sophisticated payments infrastructures of any company in the world, handling deposits and disbursements in hundreds of markets, many with different currencies. “All the innovation around payments is a means to an end — table stakes,” he said. “Uber has one of, if not the most used mobile payments methods in the world, and it was absolutely crucial — they had to do it to create the experience and service they wanted. Payment technology created certainty for riders and drivers that they’d get paid — it facilitated trust.”

Much as the true value of a retailer’s mobile payment app is in the metadata it gobbles up, the real power of digital payments lies in the largely invisible infrastructure that undergirds them. Fintech companies like Square aren’t exactly sexy, but they allow small businesses and individual merchants to process transactions without prohibitively expensive equipment or the fees that legacy credit companies charge.

“Millennials don’t trust banks, but they trust Apple and Google.”

“It’s about financial inclusion and serving real, normal people,” Reddig said. "There is a lot of opportunity to build very profitable businesses that operate better than incumbents in transparency, great design, great user experience. Millennials don't trust banks, but they trust Apple and Google."

This is already happening, just outside the U.S. If fintech’s true believers think it’ll fundamentally change the way we live, the developing world is where their vision is revealing itself most clearly. In Kenya, for example, the payment messaging service M-Pesa has attracted over 13 million monthly active users (out of a population of 44.3 million). As of last May, roughly 42% of Kenya’s GDP was transacted via M-Pesa, all without tying Kenyans to expensive, cumbersome bank accounts.

But more than that, M-Pesa has effectively invented a new form of credit that’s based on a history of reliable transactions from phone to phone, rather than through a bank. In a world where 2.5 billion people don’t have bank accounts, systems like M-Pesa are set to leapfrog Western banking the same way much of the developing world skipped the desktop and went straight to the smartphone for its computing needs. In reinventing money transfers, M-Pesa and its ilk offer more than a new way to pay — they are opportunity engines, offering the ability to build credit in a world that previously shut them out. And in the process, there are billions to be made in transfer fees.

youtube.com

By my third week, the cashless, frictionless future I’d hoped to live began to feel glitchy, burdensome, and alienating. I had to meticulously plan my every move hours or even days in advance — a haircut required me to convince my barber to start using Venmo, going out for a meal meant lining up a dining companion willing to submit to confused stares and drawn-out check-settling processes.

One January afternoon, I found myself trying to persuade a prodigiously bearded, flannel-shirt-wearing barista named Michael to allow me to pay him personally via Square Cash for a coffee, which he would then pay the register for. After a confession that this was all for a story from me and a pity laugh from him, Michael reached for his phone, but not before he locked eyes with me. “I’m only doing this because I want you to write about how much this sucks for us,” he said. He went on to talk about a popular coffee app called Cups, which allows customers to order and pay all inside the phone. “It’s like, now everyone who comes in is a robot — they just stare at their phone and wait to have their name called. Nobody even looks at us,” he said.

Charlie Warzel / BuzzFeed News

Michael, barista.

At this point, replacing my wallet with a phone struck me as little more than a shallow gimmick, an academic exercise, like living in a house mid-construction, before the appliances work and the water and electricity have been switched on: It’s entirely doable, and chances are no one’s going to get hurt, but that’s an awful reason to do anything. I needed something more drastic, which is how I found Hannes Sjoblad, who told me, with surprisingly little fanfare, that he could make me a cyborg.

When I contacted Sjoblad, whose LinkedIn profile lists him as the chief disruption officer at the Swedish biohacking group BioNyfiken, he’d been experimenting with NFC and RFID chip implants by hosting chipping parties for curious biohackers-to-be. His xNT NFC chip is really just a prototype: Sjoblad’s implantees are guinea pigs testing out what they believe could become common uses for a technology that’s usually reserved for phones and credit cards. Sjoblad himself uses his as a replacement for his house keys, business cards, and bike locks.

I asked him if I could use the chip — the same kind, more or less, that sits in and powers the Apple, Google, and Samsung Pay parts of our phones — to pay for things in a store; he wasn’t sure, but he knew a programmer who could link it to a bitcoin wallet. We Skyped once and formalized plans to make me an implantee. “I think when you meet us you'll see that we're pretty normal mainstream persons,” he told me over a grainy video chat. “We're not like some underground den of hackers.” He let out the kind of nervous, mischievous laugh you might let slip if you ran an underground den of hackers.

In the meantime, if I couldn’t bring the future to myself, I would have to do the next best thing: get into bitcoin. At its most basic, bitcoin is the very complicated product of advanced mathematics and cryptography, a “peer-to-peer system for online payments that does not require a trusted central authority.” Bitcoin can be mined by those who donate part of their computing power to help verify the peer-to-peer transactions going on in bitcoin’s ecosystem via the blockchain, which is a string of bundled past transactions. (It's a bit like if you loaned part of your computer to your bank to help it process payments across the world and got a very tiny reward for the donation). But bitcoin's real beauty, according to its disciples, is that it’s not really governed by any entity, making it nonreversible, unfreezable, and anonymous, all with very low transaction fees. It's a powerful idea, and bitcoin has been a bolded and underlined bullet point in every future-of-finance argument. But in 2016, almost eight years since its creation, using bitcoin is a world-class exercise in frustration.

Charlie Warzel / BuzzFeed News

The writer using Gyft.

If living without cards and cash meant planning all my purchases in painful detail, living without state-backed currency of any kind only exacerbated the problem. To buy anything immediately out in the physical world, I had to use bitcoin to buy gift cards and then redeem them at the store for groceries, meals, and anything else. When I ran out of toilet paper, I loaded up Gyft, a digital gift card site, and purchased a $15 CVS card, which I then redeemed for Cottonelle as the store opened — all told, a 45-minute ordeal. Splitting the bill was impossible without a friend willing to set up their own bitcoin wallet, and sending money through bitcoin's blockchain technology felt almost purposefully intimidating, with long, wonky wallet addresses, exchanges, and codes.

And again, there’s trust — using bitcoin means transferring real money into a volatile currency, which hit home when bitcoin’s value dropped almost 18% just hours after I converted $800 dollars to book a flight. Though today bitcoin is niche but somewhat stable, it’s not exactly hard to imagine the whole thing melting down overnight. (As a challenge, my editor tasked me with buying something “tangible” with bitcoin’s jokey, basically defunct cousin, Dogecoin: I was rejected by a meme memorabilia merchant on Etsy when I asked to pay for a mug with a cartoon frog using Dogecoin. A new low.)

But simply replacing paper dollars with digital ones isn’t the draw for bitcoin’s biggest advocates. Olaf Carlson-Wee, a 23-year-old early employee at the bitcoin startup Coinbase, has been living almost exclusively on bitcoin for three years. "The exciting things are not where bitcoin competes with regular money," he told me, "but where the tech is so radically different it creates new modes of behavior.” Carlson-Wee sees apps like Apple Pay as “abstraction layers,” basically just a digital copy of a common credit card — unlike bitcoin, which is a whole new platform.

Adi Chikara, a strategist for 3Pillar Global who has been advising on and investing in companies using blockchain technology for years, sees its elegant, unbreakable cryptographic security as a new way to ensure trust. In some scenarios, he argues, blockchain technology can act as a replacement for currency as a whole. Imagine a system where legal contracts are automatically executed through the blockchain — for example, your monthly car payments are directly linked to your ability to unlock your vehicle and put it in gear. The particulars are complicated, but blockchain has the potential to act as a powerful reinvention of 21st-century bartering. It’s also, ultimately, maybe the only way to ever move past a state-backed currency.

“It’s solutioneering: Take something that exists just fine and make it digital and somehow we’re all supposed to believe it’s better.”

“We had paper and it was backed by gold, and right now we're trusting the government — but with the blockchain you may not necessarily need the state,” Chikara told me. The early signs of this are around today — Circle, for example, is a peer-to-peer money transfer app, similar to Venmo, which is powered by the blockchain, meaning, unlike Venmo, the payments are instantaneous and can easily be converted into different currencies without fees.

Chikara readily admits we’re years, if not decades, away from a viable, universal blockchain-centric financial system. Like Venmo and Apple Pay and cash, bitcoin is still subject to human error, like in 2014, when the executive in charge of Mt. Gox, a popular cryptocurrency exchange, embezzled and lost hundreds of millions of dollars worth of bitcoin. But Chikara still proposes a scenario with no banks and no federal reserve.“There is no printing of money,” he said. “It's owned jointly by the people themselves, and they trust each other.” Blockchain technology is already being tested by traders across the world and has been implemented in the Australian stock exchange. IBM, Nasdaq OMX, Intel, and Cisco are exploring the blockchain and blockchain-based open ledger projects for trading, along with banks like Wells Fargo and JPMorgan. And recently Goldman Sachs filed a patent for SETLCoin, the company’s very own blockchain-powered currency.

But perhaps the best description of bitcoin’s potential came from Coinbase co-founder Fred Ehrsam, who sees blockchain technology as nothing less than the most significant open platform since the web. “We take what was once a highly controlled system and turn it into a software development problem where people can go nuts,” he said. “And it becomes like the internet, where you have a big open network, people can build whatever they want. The market decides what's good and what's not. And before you know it, you have this great big open network that has all these great ideas on it and things can really start to get interesting.”

Charlie Warzel / BuzzFeed News

Situation Stockholm.

It was the beginning of week four and bitcoin had driven me deeper into my hermetic state — most of my purchases were being made online and my relation to the real world was almost exclusively conducted through a screen of some sort. I needed a change of scenery.

As it turns out, if you yammer about the future of money long enough, somebody is likely to tell you to go to Sweden and see it for yourself. There, among the bountiful sweaters, sunless winters, and impossibly good genes, is the closest thing you’ll find to a truly cashless society. Just 20% of all consumer payments are conducted using cash in Sweden; according to a 2015 survey, only 2% of Sweden’s economy revolves around the ancient, dirty exchange of paper money and coins. I booked my flight rather painlessly using bitcoin (thanks, Expedia!) to figure out how and why 9 million polite socialists have beaten the rest of us to the paperless money future.

With its standing desks, glass-walled meeting rooms, and long corridors lined with stark black-and-white portraits, the office of Situation Stockholm looks like a startup. In fact, it’s almost the complete opposite: a 21-year-old glossy print magazine sold primarily by the city’s homeless population. The portraits on the wall are of the magazine’s vendors, who are, incidentally, some of the first pioneers of cashless street busking.

“A common response from presumptive customers was 'Sorry, I don't have any cash,'” Jenny Lindroth, an operations manager at the magazine, told me. “So we started to think of ways to take this cash business — a lot of our vendors don't have bank accounts — digital.” In 2007, Situation Stockholm started giving select vendors the ability to sell the magazine by having customers text a number, which would then add a charge to their cell phone bill. In 2013, the company bought card readers from a Swedish payment company called iZettle and sent its most reliable vendors out with them.

Charlie Warzel / BuzzFeed News

Situation Stockholm.

Since then, Situation Stockholm has seen an uptick in sales for vendors, as well as a newfound agency. “People outside the country seem to think that it’s interesting or funny that homeless people have these phones and card readers, but it's not really big news here in Sweden,” Lindroth said. “It's just common practice now — in Sweden you don't have cash.”

Walking around Stockholm’s icy cobblestoned sidewalks and winding, low-arched alleyways, I found myself ducking into countless shops, bars, and konditori cafés, eavesdropping on checkout registers and craning my neck for a peek at local wallets. Not once did I see a paper bill. Paying by phone was commonplace, and I didn’t even get a weird look when I scanned a QR code at a grocery store checkout and wordlessly strolled away with my basket of smoked meats.

According to Jacob de Geer, the CEO of iZettle, Sweden’s cashlessness can be traced back to the early 1990s, when tax subsidies encouraged citizens to buy early personal computers en masse, thereby making the country extra technologically adventurous. But all that early adoption hasn’t been easy for everyone. Swedish banks have drastically cut back on ATMs, raised cash transaction fees roughly 300% in the last four years, and made depositing as inconvenient as possible. Recently, Lindroth witnessed an elderly woman being turned away at the bank after she attempted to deposit a large amount of cash she’d been storing at home. “If she had transferred that money from her phone, she wouldn’t have been questioned in the same way.”

Charlie Warzel / BuzzFeed News

Stockholm in 2015.

The problem, according to Björn Eriksson — a former head of the Swedish police and Interpol, and a prominent dissenting voice in the country’s rush to cashlessness — is not the end of paper money, but the speed of the transition, which is especially hard on older generations, those in rural areas, tourists, and new immigrants who come to the country without cards or bank accounts. “It’s gotten so that some people are resorting to hiding money in their microwave because they have nowhere to put it,” Eriksson told me. It can even be dangerous to public health: Just last September, Sweden’s highest court ruled against the Kronoberg County Health Authority and reprimanded them for not accepting cash as legal tender for medical services in all but two of their health clinics.

Access to new technology is never evenly distributed. And even those like iZettle’s de Geer, who are enabling and profiting from a digital payments revolution, have reservations about abandoning paper money outright: “Everyone thinks I'd like to see the death of cash, but privacy is a big issue for all of us. Cash’s benefit is privacy. There's plenty that's legal to buy out there that you don't want everyone to know you've bought.” If America is headed down Sweden’s cashless path, we have much to learn from our Scandinavian friends. Or get comfortable finding stacks of twenties in the fridge next time you're at grandma’s place.

Charlie Warzel / BuzzFeed News

Chai at the Calm Body Modification clinic.

As I pushed through the door of Calm Body Modification, a bell tinkled amiably, as if to reaffirm the shop’s namesake. I looked up at the proprietors, tall men with all their exposed skin covered in tattoos. Above one, a sign advertised genital piercings for 1,000 kronor.

My piercer, Chai, and I retired to the backroom where my skewering would take place. “So now I’m going to tell you something you probably didn’t consider before,” he said, furrowing his brow. “People — very conservative right-wing Christian types — might come after you for this. They see it as the Mark of the Beast. I just want you to be prepared.” I nodded like this is something I had expected to hear.

This comes from the Book of Revelation: “And he causeth all, both small and great, rich and poor, free and bond to receive a mark on their right hand, or on their foreheads; and that no man might buy or sell, save he that had the mark, or the name of the beast or the number of his name.”

The passage essentially describes a closed economic system, where power is consolidated and financial gatekeepers can shut anyone out. It made for a potent metaphor. I’d spent the last three weeks in search of a connected, seamless future, but I found myself more separated than ever from the people around me.

Around week two, I’d noticed how robotic my interactions had become during any financial transaction: walk into some reliable big-box establishment, mumble order, flash phone, move down the line. Moments like my conversation at the coffee shop with Michael, the barista, heightened these concerns. The brick-and-mortar world of commerce is in the midst of a rewiring — one that’s supposed to bring in more merchants and give consumers more access to what they want when they want it. But that means new behaviors, some of which are likely to be harmful.

Charlie Warzel / BuzzFeed News

New commerce apps and technology may have a lower barrier to entry than, say, credit cards, but many of these programs — like miles cards — reward you and work best when you’ve got money to spend. And while much of fintech is billed as liberating us from the old ways and institutions, new gatekeepers are bound to emerge, in many respects, guiding us — perhaps unwittingly, at times — toward the outcomes that their data analysis has told them we want.

Bitcoin evangelists are optimistic, but the legacy banking system is as inescapable as it is flawed. Even today’s most disruptive money solutions are still reliant on traditional institutions. While Kenya’s M-Pesa allows money to be transferred from phone to phone outside of banks using the cellular company Vodafone’s network, at the end of the day, the transferred money is still backed by the pooled accounts held in regulated commercial banks.

Bitcoin or blockchain-based currencies could free us from the tyranny of service fees and interest rates and all the regulations that complicate and ultimately exclude merchants and large populations from the global economy. Or bitcoin could be adopted by legacy institutions that will strip the technology of its open platforms and use it to create a slick, more efficient model of the current system.

The fumes from Chai’s alcohol swab jolted me back into the moment. “OK, just a slight pinch, here,” he said. “Sometimes it helps to look away.”

Courtesy CityMD

Being chipped was oddly anticlimactic. A trip to the doctor revealed that I hadn’t done anything too horrible to myself. “Wait, you’re telling me I can unlock doors with that thing?” my physician cheerily inquired when I asked if I should be worried about my body rejecting the chip. “I might have to get one myself!” Over the course of a few weeks, the whole thing became an afterthought; a piece of me that stored information, like a low-tech flash drive that I couldn’t misplace.

But there was still the problem of payments. I reached out to former Venmo employee and co-founder Iqram Magdon-Ismail, who then enlisted the help of Nuseir Yassin, another former Venmo employee, to help me become the first person to pay for a meal with his hand.